Hong Kong registered companies have to get their finances checked through annual audits (unless the company is ‘dormant’). Under the Companies Ordinance, this rule applies to all businesses, no matter their size or whether they operate locally or internationally.

The financial audit is done by an external auditor to check the accuracy and reliability of key financial documents: the balance sheet, income statement, statement of changes in equity, and the cash flow statement.

The main purpose of an audit is to verify that your financial statements accurately reflect reality, comply with Hong Kong’s financial reporting standards, and are mathematically correct.

It’s important to note that the audit report doesn’t evaluate the health of your finances but checks for accuracy and compliance.

At the end of this process, the auditor provides a report and an opinion, which help show if the financial statements are reliable. For a detailed look at auditor’s reports in Hong Kong, click here.

The audit opinion reflects whether the financial statements are presented fairly, in all material respects, and in accordance with applicable financial reporting standards.

What is The Audit Opinion?

The audit opinion is essentially a summary of the auditor’s findings after examining your company’s financial statements.

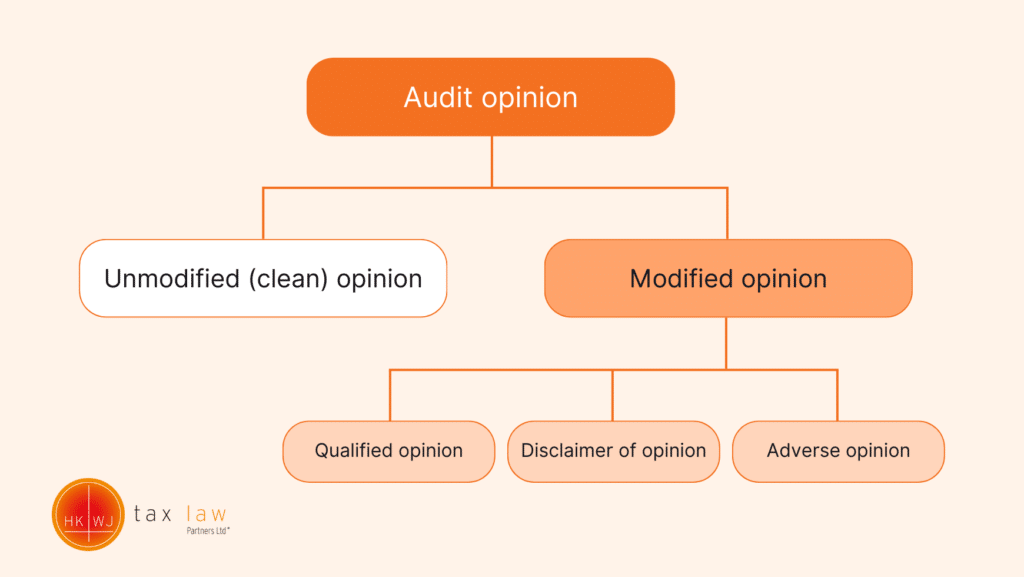

There are two main types of audit opinions: unmodified (clean) opinion and modified opinion.

An unmodified opinion means that your financial statements are clear and adhere to the required standards without any exceptions.

The auditor may add a paragraph of “Emphasis of Matter” to draw attention about a disclosure in the financial statements of which the users should be aware. The auditor can only add such a paragraph if the information about the matter is free from material misstatement.

On the other hand, a modified opinion indicates concerns about how your financial statements have been presented. This could be due to missing information or misrepresentations.

Modified opinions are further divided into three subcategories: qualified opinion, disclaimer of opinion, and adverse opinion, each reflecting different levels of issues with the financial statements.

Understanding the 4 Forms of Audit Opinions

Unmodified (clean) opinion

An unmodified opinion, often seen as a green light for the company’s financial accuracy, is issued when no significant errors or violations are found within the company’s financial report. According to the Hong Kong Auditing Standards, the auditors have gathered enough proper evidence to confidently support their opinion that the financial statements are accurate.

This type of opinion is usually expressed with phrases like, “the financial statements give a true and fair view of the state of the company’s affairs” or “the financial statements of the company are prepared, in all material aspects, in accordance with the Hong Kong Small and Medium-sized Entity Financial Reporting Standard (SME-FRS).” Such statements indicate that the financial documents are reliable and meet the required standards without material misstatements.

Achieving an unmodified opinion should be a key objective for any audit due to the potential negative consequences of a modified opinion. These include challenges such as reduced likelihood of obtaining bank loans, diminished trust from investors, and increased scrutiny from the Inland Revenue Department (IRD) during tax assessments. For an example of an Unmodified Opinion, you can view samples here from the HKICPA’s website.

Qualified opinion

A qualified opinion is issued when an auditor encounters issues during the audit that prevent them from fully verifying all aspects of the financial statements.

This might happen if there are material misstatements found, or if the auditor cannot gather enough appropriate evidence to form a completely unqualified opinion.

Despite these issues, a qualified opinion does not necessarily mean the financial statements are unreliable. It may still be considered acceptable by creditors, lenders, and investors.

However, this type of opinion will include phrases such as “except for” or “with the exception of,” followed by the specific reasons. These phrases signal that while most of the financial records are in order, there are specific areas where the information could not be fully verified, or it deviates from standard accounting practices.

Disclaimer of opinion

A disclaimer of opinion is issued when an auditor finds it impossible to complete an adequate audit of a company’s financial statements.

This situation is more severe than a qualified opinion because it arises when sufficient audit evidence cannot be obtained at all, preventing any reliable opinion on the financial statements.

Typically, this occurs if the auditor is unable to perform necessary audit procedures, often due to restrictions imposed on them or significant limitations in the company’s accounting records.

As a result, the auditor states that they “do not express an opinion” on the financial statements.

Adverse opinion

An adverse opinion is the most severe type of audit opinion and is issued when the auditor finds that the company’s financial statements fundamentally misrepresent the financial position, violating Hong Kong Accounting Standards and the Hong Kong Companies Ordinance.

This misrepresentation or inaccuracy indicates serious issues within the financial statements.

Typically, an adverse opinion will include a phrase such as “do not present fairly,” signalling that the financial statements are not only incorrect but misleading.

It suggests that the financial details provided by the company do not align with the findings of the audit, essentially indicating that the numbers do not add up.

HKWJ Tax Law Can Help

Understanding the different types of audit opinions helps your business to maintain transparency and compliance with financial regulations.

Each type of opinion provides key insights into the financial health and reporting practices of a company.

Whether you are seeking to ensure your financial statements are free from material misstatements, or you require guidance of financial audits, it is essential to have a knowledgeable and reliable auditor by your side.

If you’re looking for expert auditing services that can help safeguard the integrity of your financial reporting, do not hesitate to contact us.

Our team of experienced auditors is committed to providing the highest standard of service, ensuring your financial statements accurately reflect your business’s financial position.

Contact us today to discuss how we can assist you with your auditing needs.