As a result of an increase of foreign investments in Mainland China and a strong demand for foreign talents by local Mainland Chinese companies, many foreigners are working nowadays either permanently or temporarily in Mainland China. These foreigners are advised to do proper ahead of time tax planning or revise their employment/assignment arrangements in Mainland China and also their remuneration packages in order to achieve tax efficiency and prevent unpleasant surprises from the Mainland China Taxman due to the China individual income tax.

Mainland China Income Tax (‘IIT’) Liabilities for Individuals

According to the IIT law and regulations in Mainland China, a foreigner may be subject to IIT in Mainland China on his/her income sourced in Mainland China and/or on his/her worldwide income.

The factors relevant to determine the IIT liabilities on employment income in Mainland China include the number of days the foreigner stays in Mainland China (the threshold is generally 90 days, 183 days, 1 year and 5 years), the source of the income payment (i.e. paid in Mainland China or abroad) and the position/title the foreigner holds (i.e. top management or general employee).

Please note that in case a foreigner who stays in Mainland China for 5 successive years and for every single year, the foreigner is absent from Mainland China for not more than 30 days for a single trip or not more than a cumulative total of 90 days over a number of trips within the same year, starting from the sixth year, he/she will generally be subject to Mainland China IIT on his/her worldwide income.

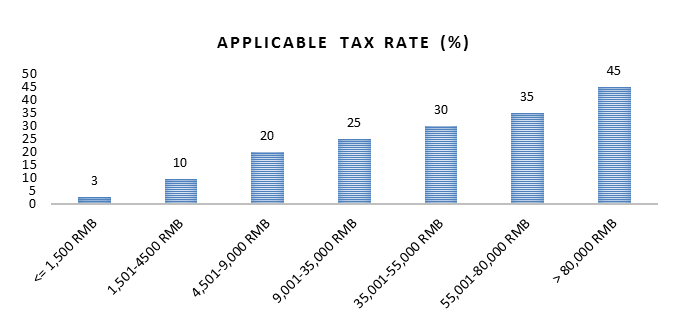

Mainland China Individual Income Tax

The employment income subject to Mainland China IIT includes salary, bonuses, allowances and other nature of remunerations in connection with the employment. In other words, the scope of the taxable income is quite broad. The taxable employment income shall be taxed at progressive rates ranging from 3% to 45% as follows:

Monthly taxable income

Tax Preferential Treatments for Foreigners

Foreigners are entitled to IIT exemption on certain employment benefits which include the following:

- Housing allowance

- Meal allowance

- Relocation benefits

- Laundry benefits

- Business trip allowance

- Language training benefits

- Children education benefits

Please note however that certain conditions have to be satisfied in order to enjoy the tax exemption on the above allowances/benefits.

One also has to note that the Mainland Chinese tax authorities have been putting more and more attention on the assessment and collection of IIT from foreigners.

It is therefore recommended to carefully examine global mobility tax issues such as the employment or assignments in Mainland China for the foreigners as well as prepare their employment contracts/assignment contracts so as to mitigate the tax risks and liabilities in Mainland China.